We’re not getting any younger. How will you be remembered?

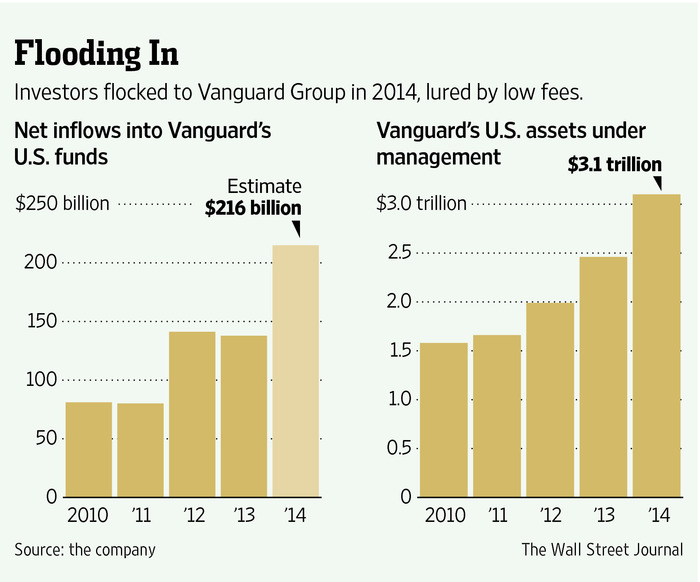

Jack Bogle, creator of low cost index mutual funds, died yesterday at 89. In Warren Buffett’s opinion, Bogle did more for the American investor than any person in the country by putting “tens and tens and tens of billions into their pockets.” “And those numbers,” Buffett added, “are going to be hundreds and hundreds of billions over time.”

As a self-taught investor, I’ve learned more from Bogle’s writing than from every other financial author combined.

Bogle’s direct, tangible legacy, low cost passive investing, is something that generations of investors will benefit from in perpetuity.

Just as generations of Pacific Northwest citizens will benefit in perpetuity from a local group’s incredibly effective activism that saved Olympia’s LBA Park from being turned into one more housing development.

A second type of legacy is less direct, tangible, and obvious; but equally meaningful. It entails living so exemplary a life that one’s descendants, and others, seek to emulate the deceased person’s attributes.

In the winter, much to the Good Wife’s dismay, I keep the house cooler than she’d prefer. Recently, when I pressed pause to think about why, it took about five seconds to realize it didn’t have anything to do with Jimmy Carter or our household’s economics. I realized it was one small way of honoring my dad’s frugality that stemmed from his Eastern Montana upbringing. A tribute of sorts. My dad never had to tell me to live below my means because he modeled it so persuasively. I want to be humble like him, just as I want to be one-tenth as generous as my mom.

Yesterday I listened to Dan Patrick interview Ian O’Connor author of Belichick: The Making of the Greatest Coach of All Time (so much for humble titles). My interest in football is waning, but Patrick is a great interviewer and O’Connor was insightful. One thing O’Connor said is that both Belichick and Brady are intensely conscious of their respective legacies.

Which got me thinking. I bet Jack Bogle was not intensely conscious of his legacy. I know for sure that Don and Carol Byrnes were not. My plan is to try to do good work, and even more importantly, be a good person, and let my legacy take care of itself. If I’m lucky, someone, sometime, will seek to emulate an attribute or two of mine.