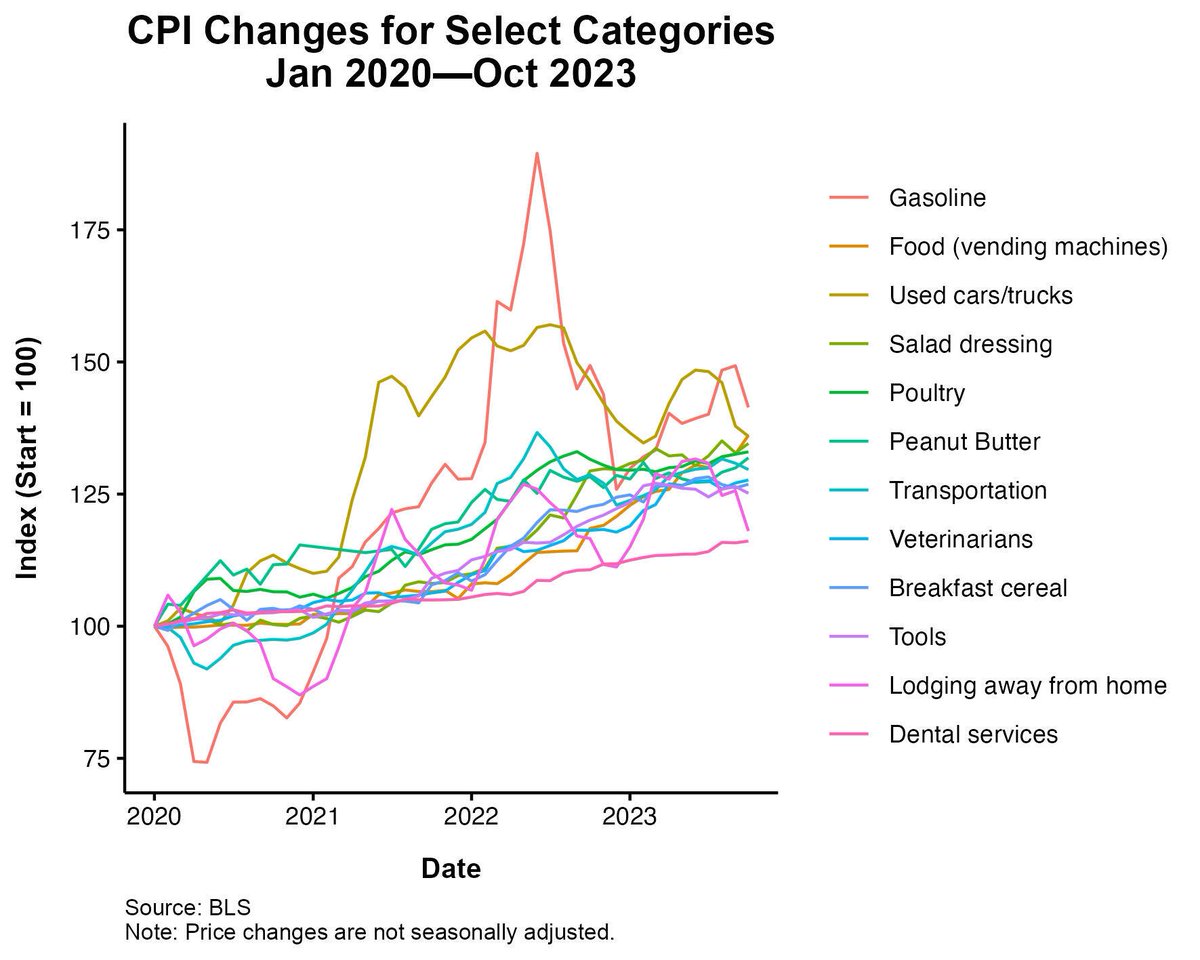

Crap graphic, not the information, the manner in which it’s depicted. Shades = mass confusion.

Crap graphic, not the information, the manner in which it’s depicted. Shades = mass confusion.

Philadelphia Attorney Tells Lawmakers How He Nearly Fell Victim to AI Scam.

How to stem the tide when high tech thieves have no exposure?

Apple’s shares slipped more than 3% in after-hours trading following last Thursday’s earnings call. Even worser, AAPL was also down Friday despite the fact that the broader market surged both Thursday and Friday.

When it comes to AAPL, I happily and knowingly break conventional personal finance wisdom that says never have more than 5% of your total invested assets in any individual stock.

Over the last fifteen years, I’ve learned to chuckle at the doubters. Chuckleheads all.

But what if I am right, until I am wrong? Maybe a little humility is in order? Maybe AAPL isn’t always going to make the personal tech of choice? If so, maybe I should pay attention to the “headwinds”.

The Wall Street Journal on Apple:

“. . . the stock already had been underperforming its big tech peers lately. Concerns were mounting over the new iPhone cycle and longer-term issues like the health of the China market and the company’s lucrative relationship with Google, which pays Apple billions of dollars every year to be the default search engine on the iPhone and other devices. That relationship is at the center of an antitrust trial against Google that has now lasted two months.

The case is a long way from resolution. China, however, is a more pressing issue. Apple’s revenue for its Greater China segment fell nearly 3% year over year compared with a 6% rise in last year’s fiscal fourth quarter. That brought China’s contribution to Apple’s total revenue to its lowest point in nearly three years. . . . Data from market research firm Counterpoint suggests the iPhone has lost momentum in China to a newly resurgent Huawei, though.”

Also, what about the anecdotal? A year ago the family had the nerve to suggest Spotify was better than Apple Music. Eventually, to save money by partnering with the GalPal, I caved and gave it a whirl. And you know what, don’t tell them, but they were right.

In related news, the sensor on the back of my Apple watch cracked. It still mostly works (no sleep data, heart rate, etc.), but I’m thinking of replacing it. And I’m leaning towards a Garmin Venu 3 or Garmin 265 because one charge lasts at least one week. How to make sense of the masses preference for Apple’s for-shits battery life? By acknowledging the company’s marketing genius.

But I digress. Back to the one, mother and father of all, AAPL warning signs. And I quote the recent CNBC headline that stopped me in my Apple track.

Jim Cramer lauds Apple’s ‘lifetime customer,’ says analysts are too negative on the company.

Harvard educated Jim Cramer is the single worst “stock guru” in the mainstream media. Yes, his television persona attracts eyeballs, but any primate throwing darts at a stock chart would outperform him.

John Oliver said it better than I ever could, “Cramer is the only person who could look you in the eye and say you are going to die tomorrow, and give you an immediate sense of calm knowing that you’re going to live for another 50 years.”

Hard to top that, but Ian Krietzberg says Cramer has been wrong so often “that Matthew Tuttle, the CEO and investment lead of Tuttle Capital Management, decided to create an ETF designed to short Jim Cramer.”

Tuttle for the win.

Maybe I should sell some AAPL and use the proceeds to buy an equal amount of SJIM.

According to the Wall Street Journal’s interpretation of the Fed’s Survey of Consumer Finances.

The gist of it:

“Rather than being left behind as all the gains in the economy accrue to billionaires, they have in fact seen bigger wealth gains over the past three years than the top 10% of families. Indeed, the biggest wealth gains between 2019 and 2022 were among the approximately 13 million families in the 80th to 90th percentile of the income distribution. Their median wealth jumped 69% from 2019, adjusted for inflation, to $747,000 in 2022.”

They note, “. . . the increase in net worth for these families has far outpaced inflation.”

They conclude:

“Rather than being swallowed by the 1%, the economy, according to these numbers, is creating a growing upper middle class. Many people got there by pursuing college degrees, steadily building retirement accounts and purchasing homes. For the most part, they became wealthy slowly, and were well-positioned when pandemic-era stimulus programs boosted asset values.”

As a result of inheriting some of their families’ growing assets, their children may very well end upper middle class too. Especially if they’re college educated.

The unreported on story of course, is the utter lack of social mobility for the other 80%, many of whom are not college graduates. Historically, the default mindset in the (dis)United States has been an assumption that each generation would enjoy a higher quality of life. Now, understandably, parents worry that their young adult children will not enjoy their level of economic security.

“Milwaukee Bucks star Giannis Antetokounmpo has agreed on a three-year, $186 million contract extension, his agent, Alex Saratsis, told ESPN on Monday.”

Giannis seems like a different cat. In lots of good ways. Most unique of all, he’s content living in Milwaukee*. Close to his family. Treats people well. The money will not dampen his competitive drive. Maybe the word is “grounded”. Good on him for not forcing a trade to a big market.

Did Saratsis get 5% or $9.3m? How much will be left after taxes. Will Giannis be able to afford his own Greek island?

*No doubt Dame Lillard makes it much more livable.

“When Mary Lou Retton, the decorated Olympic gymnast, accrued medical debt from a lengthy hospital stay, her family did what countless Americans have done before them: turned to crowdfunding to cover the bills.

NYT

On Tuesday, Ms. Retton’s daughter started a fund-raising campaign on social media for her mother, who she said was hospitalized with a rare pneumonia.

“We ask that if you could help in any way, that 1) you PRAY! and 2) if you could help us with finances for the hospital bill,” McKenna Kelley, Ms. Retton’s daughter wrote in a post on Spotfund, a crowdfunding platform similar to GoFundMe.

The public swiftly responded, with thousands donating $350,000 in less than two days, shattering the goal of $50,000.”

Another daughter did not reply when asked why her mother, with a net worth of “just $2 million”, did not have medical insurance.

I’m sure the $350,000 was the exclusive work of soft-hearted and headed liberals. Republicans are far too consistent on the whole negative consequences, tough love, and personal accountability thing to have enabled the Retton family.

A concise and cogent explanation of why Lewis’s SBF story is so problematic.

“SBF is not an effective altruist. Michael Lewis has been a literary hero of mine for decades. Liars Poker was a book that both excited me about getting into the financial services industry and also made me deeply question the motives of people in the financial services industry. So I was surprised this week to see Lewis doing a book tour and framing Sam Bankman Fried as a good person who just flew too close to the sun. He even went so far as to distance SBF from Bernie Madoff.

I have a take a deep breath here because this one actually makes me mad. SBF is exactly how most Bernie Madoff’s start. The only difference is that SBF got caught quickly. You see, most financial services ponzi schemes start with good intentions. It’s usually someone with dreams of generating huge returns running a fancy strategy that blows up. It often involves commingling client funds with firm funds. And in an effort to climb out of the hole they exploded they oftentimes make things worse. And before you know it this well-meaning person is in a financial hole so deep that they have almost no choice but to try to continue digging in the hope that no one ever asks for the shovel. In the case of SBF people asked for the shovel quickly. In the case of Bernie Madoff it took 20 years for people to ask for enough shovels to realize that he was digging with his hands.

I’m a little disheartened by the Lewis commentary because he’s trying to diminish the severity of what happened here by claiming that SBF ran a good business on one side and got into hot water in an unrelated hedge fund. Okay, but this is precisely what Madoff did. Madoff Securities was one of the largest and most innovative market makers on Wall Street for many decades. They ran a large and legitimately great business. They were also commingling client funds and running the fraud in accounts on the side. This is almost exactly what SBF was allegedly doing.

This kills me because the lack of compliance is so egregious that it’s inexcusable. I don’t care that Sam or Bernie seemed like good guys. They were negligent about compliance and commingling of funds. According to Lewis, SBF treated everything like a game inside his unregulated casino. But this is exactly why casinos (and financial firms) need to be regulated. SBF isn’t just a guy who flew too close to the sun. He’s as prone to irrationality as the rest of us and that’s why sensible regulations need to exist. There’s no excuse for this sort of thing to be happening in an age where third party firewalls are the easiest first line of defense in finance.”

File this under “Michael Lewis. . .it’s more difficult to stay on top, than to get there.”

Just because people use double negatives, it doesn’t mean they have to weight down headlines.

The headline should read, “Housing Expert: 8% Mortgage Rate likely. Less is almost always more.

“Rivian vehicles sell for over $80,000 on average. Yet they’re so expensive to build that in the second quarter the company lost $33,000 on every one it sold.”